E-invoicing in UAE

Transform Your Financial Management with e-Invoicing in UAE

Our Products:

Reverse Charge Mechanism (RCM) in UAE VAT Explained

Last updated at

December 5, 2025

Book a Demo

Learn more about this by booking a demo call with us. Our team will guide you through the process and answer any questions you may have.

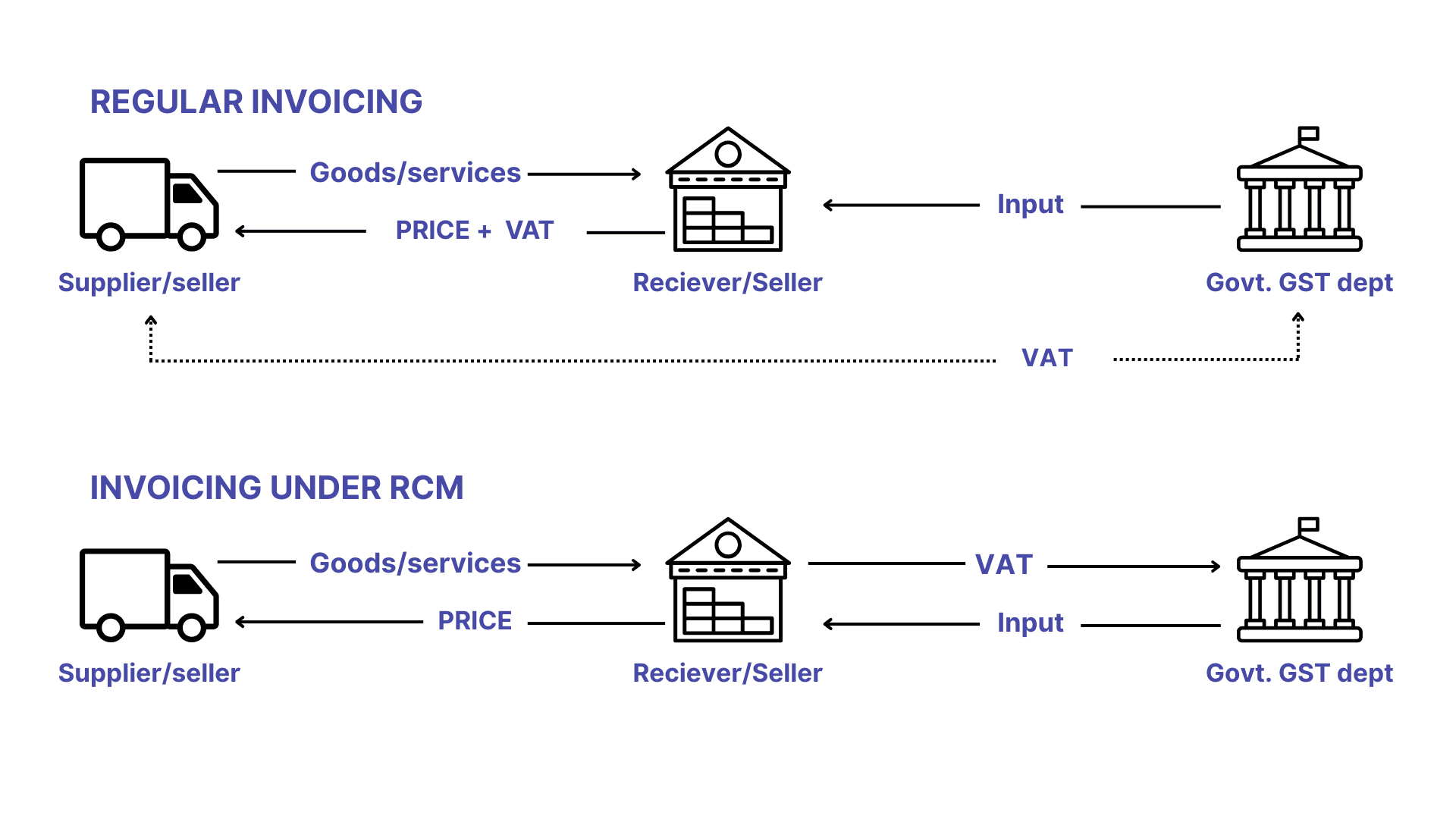

Book NowUnder the UAE VAT Law, when a registered supplier provides a taxable supply. It is their responsibility to charge VAT, collect it from the recipient, and remit to the government. This is known as the forward charge mechanism.

The following guide provides a comprehensive explanation of the Reverse Charge Mechanism within the context of UAE VAT regulations.

What is RCM in UAE VAT?

The method of collecting VAT, where the responsibility to account for VAT changes from the supplier to the recipient. It is particularly a relevant method when the supplier is not registered under UAE VAT. Also ensuring that VAT is still accounted for on taxable supplies.

As said earlier, the UAE VAT Law prescribes specific categories of supplies that fall under the scope of Reverse Charge Mechanism. In transactions involving such notified supplies, the obligation to account for and pay VAT, shifts from the supplier to the purchaser of goods or the recipient of services. This is in contrast to the forward charge mechanism, where the supplier remains responsible for the VAT liability.

The primary distinction introduced by the RCM is the transfer of tax liability from the supplier to the buyer. The government implemented the reverse charge mechanism to ensure the proper collection of VAT in situations where the supplier is not a taxable person, yet the supply takes place within the UAE. As a result, under RCM, the buyer or recipient is treated as the party making a taxable supply and is thereby required to account for and remit the corresponding VAT to the government.

Difference between regular invoicing and invoicing under RCM.

For example: SmartTech Trading LLC, a VAT-registered business in Abu Dhabi, imports smartphone accessories worth AED 8,000 from Global Gadgets Ltd, a supplier based in Singapore.

Supplier, ie, the Global Gadgets Ltd, issues an invoice for AED 8,000 without charging VAT.

The buyer, ie, SmartTech Trading LLC, calculates VAT at 5% of AED 8,000, that is, AED 400.

SmartTech Trading LLC records this AED 400 VAT as both:

- Output VAT (payable) to the FTA

- Input VAT (recoverable), if eligible, in the same VAT return.

The transaction is recorded, in the VAT Return Form 201, under the relevant reverse charge sections (Boxes 3, 6, and 10).

It should be noted that the buyer is in charge of figuring out, declaring, and paying the VAT directly to the FTA even when the supplier is located abroad and is not registered for VAT in the UAE.

Legal Framework for RCM in UAE VAT

Federal Decree-Law No. 8 of 2017 on Value Added Tax serves as the foundation for the UAE VAT system's Reverse Charge Mechanism (RCM). Article 48 provides a detailed explanation of it. The circumstances under which the RCM is applicable are outlined in this law.

The onus of paying VAT passes from the provider to the buyer under the RCM. This normally occurs when the provider is located outside of the UAE. The VAT must be calculated and paid immediately to the Federal Tax Authority by the UAE company that receives the products or services.

Even for imports from non-resident providers that aren't registered for VAT in the UAE, this method guarantees that VAT is collected correctly.

Supplies Subject to the Reverse Charge Mechanism (RCM) under UAE VAT

The UAE VAT Law specifies certain supplies that are subject to the Reverse Charge Mechanism and has outlined specific conditions for their application within the UAE Executive Regulations.

- Import of goods and services for business purposes

- Applicable when taxable goods or services are imported into UAE from other GCC or non-GCC countries.

- The supplier must be located in another country and may or may not have a business presence in the UAE.

- Purchase goods from a designated zone: When taxable goods are acquired from a designated zone within UAE.

- Supply of specific energy and natural resources:

- Hydrocarbons supplied to a registered recipient in the United Arab Emirates for resale, by a registered supplier.

- Delivery of crude or refined oil, to a registered recipient in the United Arab Emirates by a registered supplier.

- Natural gas, either processed or unprocessed, supplied to a registered recipient in the United Arab Emirates by a registered supplier.

- Production and distribution of any form of energy supplied by a registered supplier to a registered recipient in the UAE.

- Non-Resident's Supply of products or Services: When someone who doesn't live in the United Arab Emirates provides products or services to a taxable person who is based there.

- Transactions Involving Gold and Diamonds

- Supply of gold and diamonds.

- Purchase of gold and diamonds for resale or further manufacturing or production.

- Exclusions from RCM Applicability: The reverse charge mechanism does not apply to:

- The export of gold and diamonds.

- The supply of investment precious metals (platinum or gold with a purity of 99% and - above, tradable in global markets).

- The export of products where the principal component is gold or diamonds.

Note that, in order for the reverse charge rules to be applicable, each of the above mentioned supply categories, must meet certain requirements outlined in the UAE VAT Executive Regulations.

Advantages of Reverse Charge Mechanism

- In the UAE, foreign suppliers are no longer obliged to register for VAT, because of the Reverse Charge Mechanism. By reducing administrative requirements and simplifying regulatory procedures, for non-resident enterprises, this promotes international trade.

- By assigning the responsibility of accounting for VAT, to the UAE-based recipient, the mechanism safeguards against potential tax evasion. This approach ensures that VAT is duly collected and reported within the UAE. This reduces the possibility of fraudulent claims from non-resident suppliers.

- For companies who import products and services into the United Arab Emirates, the system streamlines VAT procedures. It makes the international trade by allowing local companies to do deals with foreign suppliers without having to cope with the difficulties of UAE VAT registration.

Challenges of Reverse Charge Mechanism

- Companies must be thorough and have a clear understanding of when and how the RCM affects their transactions. For businesses engaged in different cross-border dealings, it can be very complex. This makes it necessary for careful VAT administration and compliance procedures.

- Mistakes in VAT reporting or failure to account for VAT can lead to penalties and regulatory issues. It take meticulous attention to detail and constant compliance with the relevant tax laws, to guarantee correctness in VAT treatment under RCM.

Procedures for the business to ensure compliance with the RCM

To remain compliant with the RCM provisions, under the UAE VAT regulations, businesses should adhere to the following procedures:

- Verify VAT registration status: In order to apply the reverse charge provisions, make sure the recipient entity is properly registered for VAT in the United Arab Emirates.

- Determine whether transactions are relevant: Examine every purchase transaction carefully to see if it is covered by RCM. Pay close attention to imports and products or services that are specifically mentioned in the appropriate RCM rules.

- Maintain Comprehensive Documentation: Retain accurate and detailed records of all transactions subject to RCM, ensuring that invoices and supporting documents explicitly indicate the application of the reverse charge.

- Ensure Correct VAT Reporting: Fulfill your regulatory responsibilities by accurately recording RCM-related transactions, in your VAT returns and, if necessary, accounting for both output VAT and the accompanying input VAT.

- Seek Professional Advisory Support: Engage qualified VAT consultants or tax advisors to assist in managing complex RCM transactions and to ensure full compliance with UAE VAT legislation.

Obligations under the RCM

The buyer of products or the recipient of services is now responsible for paying VAT to the government under the RCM. As a result, the accountable party must carry out the following obligations:

- Determine the correct value of supply upon which VAT is to be calculated.

- Accurately account for the VAT payable on transactions subject to the reverse charge within the business’s VAT records.

- Ensure timely payment of the applicable VAT amount to the FTA in accordance with statutory deadlines.

- Claim input tax credit on reverse charge supplies, subject to the eligibility criteria set out under UAE VAT regulations.

- Keep detailed documentation as evidence of tax payment and to substantiate any input tax claims made in relation to reverse charge transactions.

Conclusion

In the United Arab Emirates, businesses subject to the Reverse Charge Mechanism for Value Added Tax compliance, typically don't require a specific standalone form. Instead, RCM-related transactions are reported within the standard VAT Return Form 201. To get the most current and relevant forms or guidelines, businesses should consult the Federal Tax Authority's official website. The FTA provides a comprehensive repository of VAT-related resources, including guides, public clarifications, and any necessary forms.

Quick Navigation

Book a Demo

Learn more by booking a demo with our team. We'll guide you step by step.