E-invoicing in UAE

Transform Your Financial Management with e-Invoicing in UAE

Our Products:

UAE Tax Credit Note: Examples, Formats & Benefits Explained

Last updated at

December 6, 2025

Book a Demo

Learn more about this by booking a demo call with us. Our team will guide you through the process and answer any questions you may have.

Book NowA Tax Credit Note is a document a supplier issues to reduce or cancel the value of a previously issued tax invoice. It applies when goods are returned, consideration is revised, or VAT was charged incorrectly. Issuing a Tax Credit Note ensures that Output Tax and Input Tax are correctly adjusted in the VAT returns of both parties.

This guide covers when to issue a Tax Credit Note, the required data fields, its impact on VAT reporting, the approved format, and rules for electronic issuance.

What is a UAE Tax Credit Note?

A Tax Credit Note is a written or electronic document a supplier issues to reduce or cancel the value of a previously issued tax invoice. It adjusts the VAT charged on a taxable supply to ensure accurate reporting for both the supplier and the recipient.

The supplier reduces Output Tax, and the buyer adjusts Input Tax in their VAT returns for the relevant period. Credit notes typically arise from returned supplies, revised pricing, or overstated VAT.

Example for Tax Credit Note

Al Masa Stationery LLC, a VAT-registered supplier in Dubai, delivered a batch of office supplies to Vision Consulting at a value of AED 12,000 plus AED 600 VAT. After receiving the order, the client returned items worth AED 3,000 due to damage. To adjust the value of the original supply, Al Masa Stationery issued a Tax Credit Note for AED 3,000 and AED 150 VAT. This will ensure that both the supplier and the customer reflect the corrected values on their VAT returns in line with the UAE VAT Law.

When Must You Issue a Tax Credit Note?

A VAT-registered supplier will issue a Tax Credit Note when the Output Tax of a previous taxable supply must be reduced due to a correction in the consideration or the VAT amount on the original tax invoice.

The UAE VAT Law requires a Tax Credit Note in the following situations:

- The supply is cancelled after the invoice has been issued

- The nature of the supply changes, affecting its tax treatment

- The consideration is reduced, such as through post-supply discounts

- The recipient returns goods or services, fully or partially

- VAT was charged incorrectly, such as using the wrong rate or place of supply

Mandatory Data Fields in a Tax Credit Note

A VAT-registered supplier must include the required data fields on a Tax Credit Note to meet the rules of UAE VAT regulations. These fields make the document valid for VAT return adjustments and suitable for audits.

A valid Tax Credit Note must include:

- The title “Tax Credit Note”

- The supplier’s name, address, and Tax Registration Number (TRN)

- The recipient’s name, address, and TRN (if available)

- A unique sequential number for the credit note

- The date of issue

- A reference to the original tax invoice being adjusted

- The reason for issuing the credit note (e.g., returns, discount, correction)

- A description of the goods or services involved

- The amount of reduction in the taxable value

- The VAT rate applied

- The amount of VAT reduced

- The total value of the credit note, including VAT

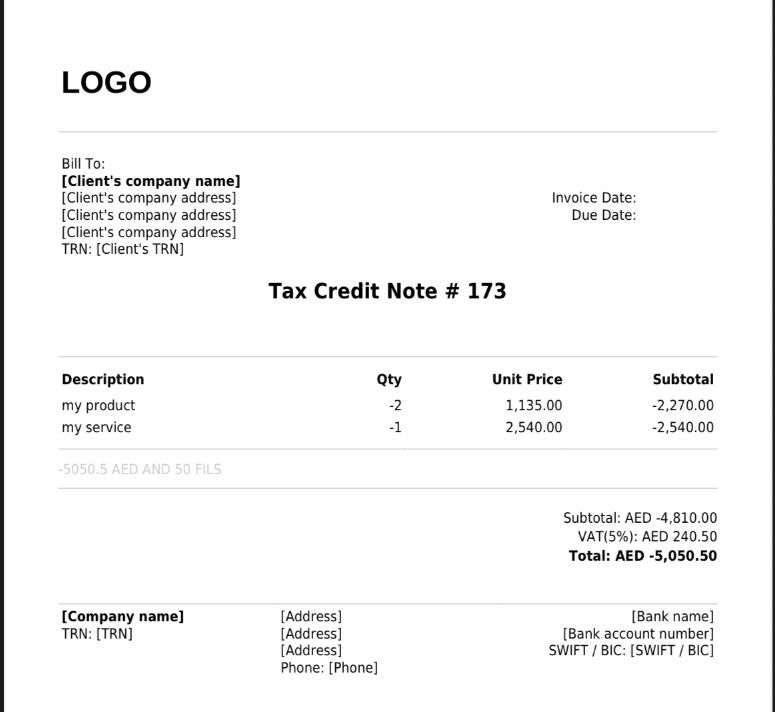

UAE Tax Credit Note Format

Here below is the format of a UAE-compliant Tax Credit Note:

How a Tax Credit Note Affects VAT Reporting

A Tax Credit Note adjusts the VAT already reported in a previous return. It reduces the Output Tax for the supplier and the Input Tax for the recipient in the tax period in which the credit note is issued or received.

If the original Tax Invoice was already reported, the supplier must declare the reduced Output Tax in the return for the period when the credit note is issued. The recipient must reduce the Input Tax in the same period the credit note is received.

For deemed supplies, the supplier must still adjust the Output Tax and retain the credit note for audit.

Issuing Tax Credit Notes for Deemed Supplies

In the case of a deemed supply, where no actual recipient exists, a VAT-registered supplier must still issue a Tax Credit Note if the Output Tax needs to be reduced.

Although the supply does not involve a sale to a buyer, the VAT Law requires the supplier to issue a Tax Credit Note and retain a copy as part of the tax records. This will ensure a correct adjustment of the Output Tax and maintain traceability in case of an audit or a tax review.

Deemed supplies typically include:

- Business assets used for non-business purposes

- Goods held at the time of VAT deregistration

- Transfers of goods across GCC branches (non-taxable movements)

- Supplies made without consideration

If a supplier accounts for Output Tax on a deemed supply and later becomes eligible for an adjustment due to a cancellation, an error, or a change in value, the supplier must create a Tax Credit Note. The document must include all mandatory fields under the VAT Law. The supplier will not deliver this note to a recipient but will keep it internally as part of the compliance records.

Electronic Tax Credit Notes

A VAT-registered supplier can issue a Tax Credit Note in electronic form if it meets the conditions set by UAE VAT Law. The electronic note must:

- Include all mandatory fields

- Be authentic, complete, and readable

- Be securely stored and easily retrievable

- Remain accessible to the FTA for audit or review

The system used must clearly link the credit note to the original tax invoice and maintain a reliable audit trail. Electronic credit notes carry the same legal weight as paper-based ones but must fully comply with format and record-keeping standards. If not, the FTA may treat the document as non-compliant.

FAQs

1. When will a business issue a Tax Credit Note under UAE VAT?

When a VAT-registered business needs to reduce previously reported Output Tax due to supply cancellation, value reduction, return of goods/services, or an error in VAT charged.

2. What is the purpose of a Tax Credit Note in VAT reporting?

To adjust VAT already reported. It reduces the supplier’s Output Tax and the recipient’s Input Tax in the period the credit note is issued or received.

3. Is a Tax Credit Note mandatory for deemed supplies?

Yes. Even without a buyer, the supplier must issue and retain the credit note to adjust Output Tax and meet audit requirements.

4. Can a Tax Credit Note be issued electronically in the UAE?

Yes, if it includes all required fields, remains readable, and is securely stored with audit traceability.

5. What happens if I don’t issue a Tax Credit Note when required?

You may face penalties, VAT reassessment, or audit issues for non-compliance.

6. Do I have to deliver the Tax Credit Note to the customer?

Not in all cases. For deemed supplies, you can retain the credit note without delivery, as long as it’s complete and audit-ready.

Quick Navigation

Book a Demo

Learn more by booking a demo with our team. We'll guide you step by step.