E-invoicing in UAE

Transform Your Financial Management with e-Invoicing in UAE

Our Products:

Understanding VAT in the UAE: Key Rates, How to Register & Exemptions

Last updated at

March 12, 2026

Book a Demo

Learn more about this by booking a demo call with us. Our team will guide you through the process and answer any questions you may have.

Book NowUnderstanding VAT in the UAE: Key Rates, How to Register & Exemptions

To strengthen and diversify the economy, beyond oil revenues, the UAE introduced Value Added Tax or VAT on January 1 2018. It is implemented under the Federal Decree Law No:8 of 2017. Since then, VAT has become an important part of business operations, consumer transactions, and economic activities across all Emirates.

This in-depth guide includes:

✅ Latest VAT rules in UAE & rates & (2025 changes)

✅ VAT calculation

✅ Step-by-step registration (for new companies)

✅ E-invoicing & digital tax reporting

✅ VAT refunds for tourists

✅ Penalties for non-compliance

VAT in UAE?

A consumption-based tax known as Value Added Tax (VAT) is applied to the added value of products and services at each level of the supply chain, from production and distribution to the point of sale. The final cost is ultimately borne by the end user, even though firms collect and pay VAT along the process.

VAT is applied and documented at every level of the supply and distribution chain; unlike traditional sales tax, which is only collected at the point of sale.

Under Federal Decree Law No. 8 of 2017, the UAE imposed VAT on January 1, 2018, and the rate will remain at 5% until 2025. Within 28 days at the end of their tax period, all registered businesses must submit their VAT returns using VAT form 201.

UAE VAT Rates

Standard Rate (5%): The standard VAT rate in the UAE is 5%, applicable to most of the goods and services.

This includes;

- Retail sales of goods

- Professional services

- Commercial property rentals

- Food and beverages

- Utility services

- Electronic services

- Imported good

Zero Rate (0%): Zero-rated supplies are subject to 0% VAT, enabling Companies to reclaim the input VAT they paid on their purchases even if they are using zero-rated suppliers. In the United Arab Emirates, the following supplies are zero-rated:

- Exports of goods and services

- International transportation

- Certain educational and healthcare services

- Natural gas and crude oil supplies.

Exemptions:

Exempt supplies are not subject to VAT; however, businesses cannot recover input VAT incurred on these transactions. Exempt supplies in the UAE include:

- Selected financial services that are paid for with spreads or implicit margins (instead of explicit fees)

- Residential structures, whether for sale or lease, excluding zero-rated

- Undeveloped property (land devoid of any fully or partially constructed structures)

- Local services for passenger transportation

How is Vat calculated in UAE?

The following formula is used to calculate VAT in UAE.

Net VAT payable= Output VAT - Input VAT

- VAT collected on the sales is Output VAT

- -VAT paid on business purchases is Input VAT.

Example:

Step 1: Calculate Input VAT (on purchases)

For example, if you spend AED 1,000 on goods that are subject to 5% VAT.

Input VAT: 1,000 multiplied by 5% equals AED 50.

Step 2: Calculate Output VAT (on sales): For example, sell products for AED 2,000 and charge 5% VAT. Output VAT = 2,000 x 5% = AED 100.

Step 3: Calculate Net VAT Payable. Net VAT is Output VAT minus Input VAT, which equals AED 50.

Step 4: Add VAT to the Net Price:

Total Price = Net Price x (1 + VAT Rate)

For example, if the net price is AED 200, the total price is AED 210, calculated as 200 multiplied by 1.05.

How to Calculate 5 VAT in UAE?

To calculate 5% VAT:

Amount of VAT = (Price × 5) ÷ 100

Price + VAT Amount equals Total Price Including VAT

If a product costs 1,000 AED, for example:

(1,000 × 5) ÷ 100 = AED 50 = 1,000 + 50 = AED 1,050 VAT

To subtract VAT from the gross price, use the formula:

Net Price = Gross Price/(1+VAT Rate).

For example, if the gross price is AED 210, the net price is AED 200 (210 divided by 1.05).

How does VAT work in UAE?

At every step of the supply chain in the UAE, from the manufacturer to the wholesaler to the retailer, businesses charge VAT on sales (Output VAT) and pay VAT on purchases (Input VAT).

The difference between the VAT collected on sales (output tax) and the one paid on purchases (input tax) is what each business either pays to the government (if output tax is more) or claims as a refund (if input tax is more).

This system creates tax credit chain where each business can deduct the VAT they paid from the VAT it collected, so tax is only applied on the "value added" at each stage.

Example:

A factory sells a table to a store for AED 1000 + AED 50 VAT (that is 5%).

The factory's output tax will be AED 50. Factory remits this AED 50 to the government (if no input tax to offset).

Now a store buys this table for AED 1050 and they adds the value by selling it for AED 1500 + AED 75 VAT. Now the store's output tax will be AED 75 and their input tax will be AED 50 (VAT paid when buying the table). The store pays AED 75 reducing AED 50 from it. And they pays AED 25 to the government. That is, the tax is applied only on the value that is added (AED 450) by the store.

VAT Registration in UAE

Mandatory registration

In UAE, businesses are required to register for VAT if the total value of their taxable supplies and imports exceeds AED 375,000 within 12 months.

- Taxable supplies = Sales of goods or services that are subject to VAT

- Imports = goods or services brought into the UAE.

What happens if a business fails to file VAT?

If exceeded, businesses are required to file VAT with the FTA within 30 days of exceeding the threshold. Failure to register within the timeline incurs a penalty of AED 10,000.

Example:

Suppose a business in UAE makes AED 300,000 in taxable sales by July. In August, it makes an additional AED 100,000 in taxable sales, making it a total of AED 400,000. In this case, they have crossed the limit of AED 375,000 in August. Therefore, the business is to mandatorily apply for VAT by September (within 30 days of crossing), and failing to do so, FTA charges AED 10,000 as a fine/penalty.

Voluntary Registration

Businesses can opt for voluntary registration if their taxable supplies and imports exceed AED 187,500.

Note: Payments must be made through the FTA's EmaraTax portal, using options such as credit card, local bank transfer (GIBAN), eDebit, or e-Dirham card. Payment deadlines are strict.Late payment or non-payment results in fine/penalties.

VAT Filing in UAE

Filing Frequency

Quarterly: Applicable for business with annual turnover less than AED 150 million

Monthly: Applicable for businesses with annual turnover exceeding AED 150 million.

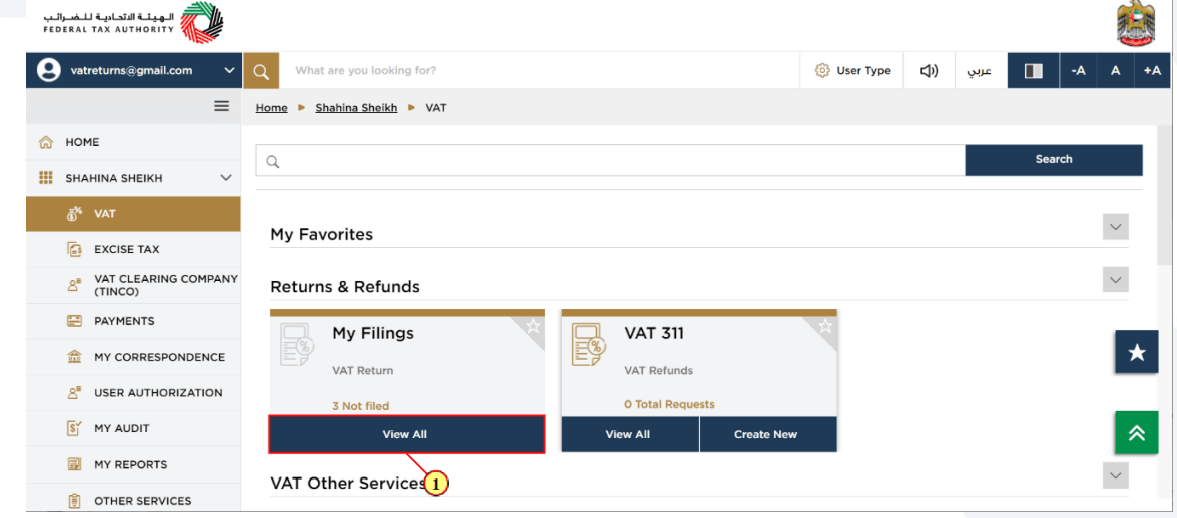

The ‘view all’ option under ‘My filings’ will allow you to select the period you are filing for. To continue, click on ‘file’ option against the period you have chosen

Filing Process

- Log in to FTA Portal (Click here): Use your Tax Registration Number (TRN).

- Prepare Records: Maintain accurate records of input and output tax.

- Submit VAT Return: File returns by the 28th of the month following the tax period (VAT form 201)

- Make Payment: Ensure timely payment to avoid penalties.

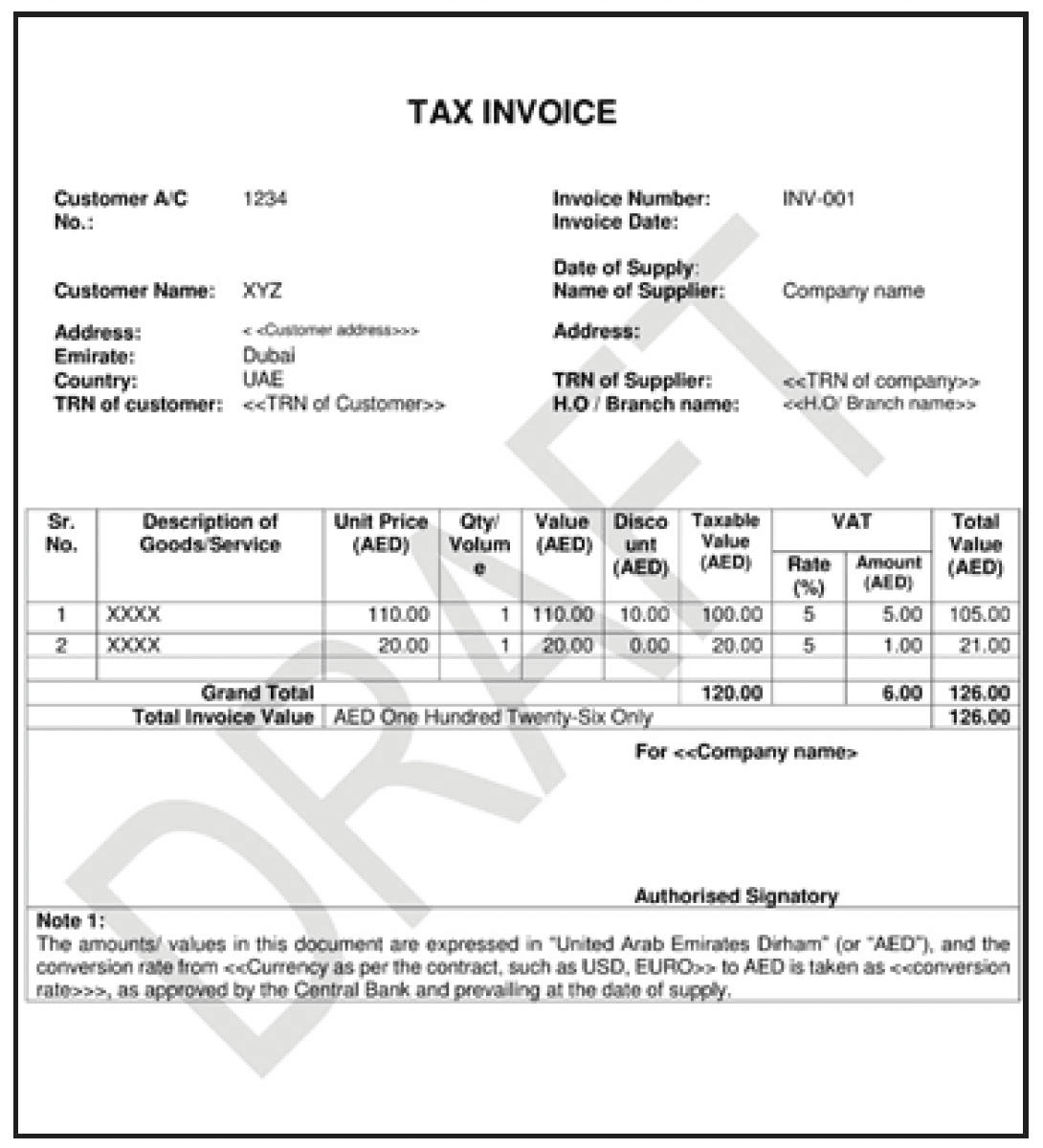

VAT Invoice Format in UAE

A valid VAT invoice must include:

- Supplier's name, address, and TRN

- Recipient's name and address

- Unique invoice number

- Date of issue

- Description of goods or services

- Quantity and unit price

- Applicable VAT rate and amount

- Total amount including VAT

Format of VAT invoice in UAE.

UAE VAT Reverse Charge Mechanism

The Reverse Charge Mechanism in UAE (RCM) transfers the buyer's obligation to pay VAT from the provider, mainly in:

- Imports: The products or services which are brought into the GCC region from abroad.

- Industries: By 2025, RCM will include more precious metals and other stones such as gold, diamonds, pearls, rubies, sapphires, and emeralds.

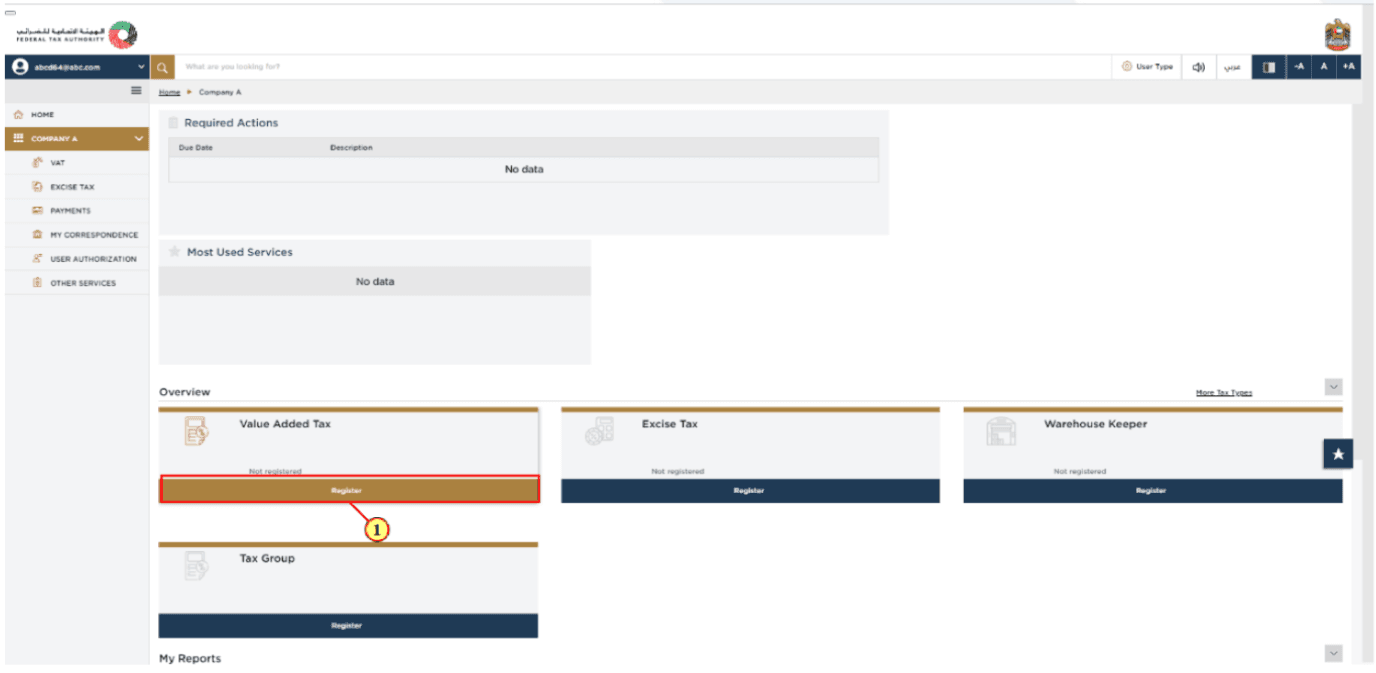

How to Register for VAT in UAE for a New Company

If your business is new to the UAE and you anticipate your taxable supplies to surpass AED 375,000 then A VAT registration is compulsory. If above AED 187,500, it can be voluntary.

Step-by-Step Process:

1. Create an EmaraTax Account (FTA Portal)

Login to the Federal Tax Authority (FTA) Portal (EmaraTax platform). Click "Sign Up" and sign up with your email address, and mobile number.

2. Log in to EmaraTax

Once registered, log in to your dashboard to start the VAT registration process.

3. Create a Taxable Person Profile

Before applying, you need to create a ‘Taxable Person’ profile with your business type (Legal person – e.g., LLC, or Natural person – freelancer/sole proprietor).

4. Initiate VAT Registration

Navigate to “VAT” > “Register”.

Fill in details such as:

- Business activities

- Expected turnover

- Imports/Exports

- Customs registration (if applicable)

5. Upload Required Documents

Here are the key documents usually required:

| Trade License | Mandatory |

| Passport Copy of Owner | Mandatory |

| Emirates ID of Owner/Manager | Mandatory |

| Memorandum of Association | If applicable |

| Bank Account IBAN Letter | For refund purposes |

| Business Contact Details | UAE address, email, mobile |

| Projected Financials or Invoices | If newly started |

6. Review and Submit

Double-check all your entries and submit the VAT registration form.

You will receive an acknowledgment from the FTA.

7. Receive TRN (Tax Registration Number)

If everything is in order, you’ll receive your TRN within 20 business days (sometimes earlier).

Once approved, your company is officially VAT registered.

Important Notes for New Companies:

- Estimate your turnover realistically – FTA may ask for justification.

- Keep all documents scanned and clear (PDF/JPG formats under 2MB).

- Failing to register within 30 days of becoming eligible may lead to a AED 10,000 fine.

Penalties for VAT Non-Compliance in the UAE

The UAE imposes strict penalties for VAT violations, including fines for late registration, filing, or payment, improper record-keeping, and other infractions. A detailed penalty schedule is available within the full guide.

As of 2025, here is a summary of some common VAT penalties in the UAE:

| Violation | Penalty amount |

| Failure to register VAT (within 30 days) | AED 10,000 |

| Failure to deregsiter (within the given time limit) | AED 1,000 per month (max AED 10,000) |

| Late VAT return filing | AED 1,000 (first offense) AED 2,000 ( if repeated within 24 months) |

| Late VAT payment | 2% of unpaid tax immediately after due date; 4% after 7 days; 1% daily after 1 month (max 300% of unpaid tax) |

| Failure to maintain proper records | AED 10,000 - first time AED 50,000 - if repeated within 24 months |

| Incorrect VAT return filing | AED 3000 - first time AED 5000 - if repeated within 24 months |

| Failure to issue VAT invoice/credit note | AED 5000 per missing/incorrect invoice |

| Incorrect information submitted to FTA | AED 3000 - first time AED 5000 - if repeated within 24 months |

| Not displaying prices inclusive of VAT | AED 5000 |

| Failure to notify FTA of margin scheme use | AED 2500 |

| Failure to facilitate FTA audit | AED 20000 |

| Failure to comply with Designated Zone transfer procedures | More than AED 50,000 or 50% of unpaid tax on goods |

| Failing in account for tax on imported goods | 50% of unpaid or undeclared tax |

| Not submitting records in Arabic when requested | AED 20000 |

| Failure to notify amendment of tax records | AED 5000 - first time AED 10000 - if repeated |

| Not issuing e-invoices/credit notes | AED 2500 per violation |

| Voluntary disclosure (error less than AED 10,000) | Can correct in next VAT return |

| Voluntary disclosure (error more than AED 10,000) | Notify FTA within 20 days; AED 1,000 (first); AED 2,000 (repeat); plus 5–40% of tax difference based on delay duration |

| Failing to inform FTA about any tax errors before FTA notification/audit | 50% of error, plus 4% monthly on underpaid tax |

| Failure to account for tax on behalf of another person | 2% daily for first day, 4% monthly thereafter (up to 300%) |

How to claim VAT refund in UAE for tourists?

Tourists may claim VAT refunds when:

- Goods are purchased from retailers participating in the Tax Refund for Tourists Scheme.

- Goods are shipped within 90 days from the time they were purchased.

- The tourist presents a valid passport and boarding pass.

- Refunds can be claimed at designated refund points across the UAE.

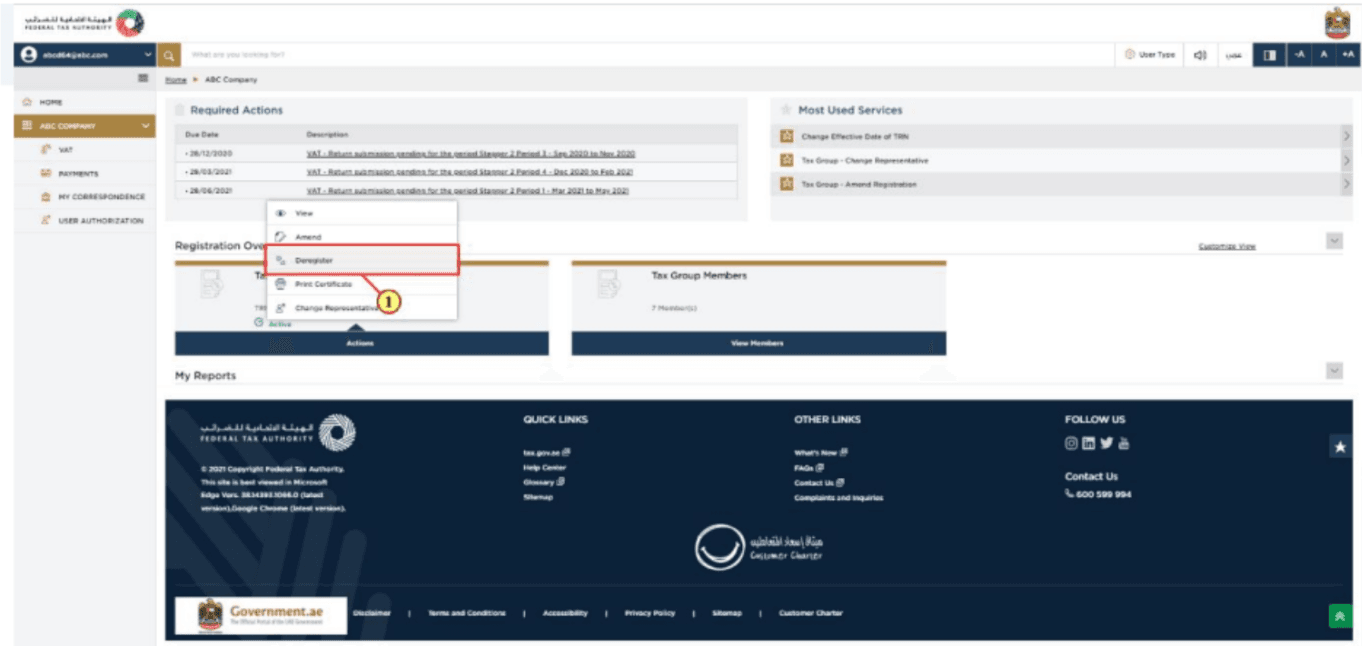

VAT Deregistration in UAE

Businesses must apply for VAT deregistration if:

- They cease making taxable supplies.

- Their taxable turnover falls below the voluntary registration threshold.

Applications should be submitted through the FTA portal, with all outstanding VAT liabilities settled prior.

Select ‘Deregister’ to initiate the Tax Group Deregistration application.

UAE VAT Consultants

Compliance can be ensured by hiring a VAT consultants in UAE, particularly for companies handling intricate transactions.

Specialized consultants offer services including:

- VAT registration and deregistration

- Return filing and record maintenance

- Advisory on transaction VAT implications

- Employee VAT compliance training

UAE VAT Registration Deadline

After being eligible, businesses have 30 days to register for VAT. Penalties for late registration might reach AED 10,000.

Required Documents for UAE VAT Registration:

- Trade license

- Passport and Emirates ID of the owner

- Memorandum of Association

- Bank account details

- Financial statements

- Customs registration (if applicable)

Special VAT Considerations in UAE

VAT Recovery and Refund

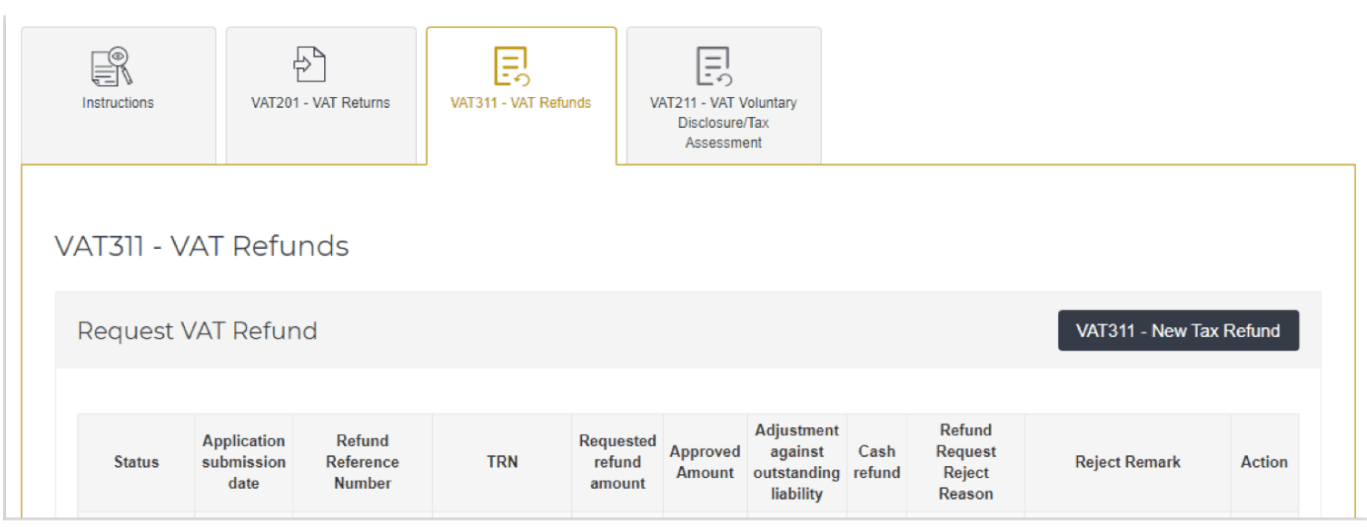

Excess input VAT over output VAT is reclaimable via the VAT 311 form. The FTA will assess refund claims within 20 business days and advise the taxpayer of its decision to accept or reject them. Once accepted, the refund will be given out within five business days.

Special VAT Considerations in UAE

VAT Recovery and Refund

Excess input VAT over output VAT is reclaimable via the VAT 311 form. The FTA will assess refund claims within 20 business days and advise the taxpayer of its decision to accept or reject them. Once accepted, the refund will be given out within five business days.

Zero-Rating Export of Services

a provision that applies a 0% tax rate to taxable services, allowing businesses to recover input VAT on associated expenses. For companies exporting services outside the UAE, this can result in significant cost savings by enabling VAT recovery while exempting their services from output tax.To be eligible for zero-rating, the following requirements must be met

- The service recipient's place of residence must not be in the UAE.

- Physical Presence of the receiver: The receiver must typically be located outside of the UAE when the service is done. If the beneficiary is temporarily present in the UAE for fewer than 30 days, zero-rating may still apply, assuming their presence is unrelated to the service.

- Service Type: Some services are exempt from zero-rating due to their nature.

VAT for tourists.

Tourists visiting the UAE must pay VAT at the point of sale, however they may be eligible for refunds on purchases made within the nation. This strategy promotes tourism and ensures tax collection.

How to Claim VAT on Imported Goods in UAE

For imported goods:

- VAT is typically accounted for under the Reverse Charge Mechanism.

- Businesses must declare imports in their VAT returns and can claim input VAT, subject to eligibility.

How to File VAT Return in UAE

VAT returns should be submitted through the FTA portal (EmaraTax platform) by 28th day following the end of tax period (monthly/quarterly) by filing VAT return document (VAT form 201). Be sure to have all of your papers in order, and pay on time so that you avoid penalties.

Conclusion

Staying compliant with VAT regulations in the UAE means not only filing accurate VAT returns on time but also preparing for the country’s upcoming mandatory e-invoicing requirements. As the FTA moves towards full digital tax administration, adopting a reliable, accredited e-invoicing solution is essential for every VAT-registered business.

Flick is an officially accredited e-invoice service provider in the UAE, offering seamless, FTA-compliant solutions to help businesses stay ahead of regulatory changes. To learn more and get started, visit us now.

Quick Navigation

Book a Demo

Learn more by booking a demo with our team. We'll guide you step by step.