E-invoicing in UAE

Transform Your Financial Management with e-Invoicing in UAE

Our Products:

Step-by-Step VAT Return Filing in UAE (FTA Guide)

Last updated at

December 5, 2025

Book a Demo

Learn more about this by booking a demo call with us. Our team will guide you through the process and answer any questions you may have.

Book NowVAT Return Filing Process in the UAE: Complete Step-by-Step Guide

If you run a business that is registered for VAT in the UAE, you will file a VAT return for each tax period as per the rules of the Federal Tax Authority and this blog will explain the full process of filing a VAT return in the UAE.

What is a VAT Return in the UAE?

A VAT return is a report that a registered business will submit to the Federal Tax Authority. It shows the amount of VAT the business collected on the sale of goods or services and the amount it paid on purchases during a tax period. It also includes details of imports, exports, exempt sales, and zero-rated transactions.

The purpose of this return is to calculate the final VAT position:

- If the business collected more VAT than it paid, it must pay the balance to the FTA.

- If the business paid more VAT than it collected, it can request a refund or carry the excess forward.

In the UAE every registered business will file a VAT return using Form VAT 201 through the EMARATAX portal and the filing will take place on a monthly basis or on a quarterly basis depending on the value of the business turnover.

VAT Return Obligation Based on Turnover

A business will file a VAT return if it holds a valid VAT registration in the UAE. The Federal Tax Authority sets two main thresholds.

A business must register and file VAT returns if the value of its taxable turnover goes above AED 375,000 in a year.

A business can register on a voluntary basis if the value of its taxable turnover or expenses goes above AED 187,500 and once registered it will file VAT returns for each tax period.

A business must file a VAT return even if it makes no sales or purchases during the period. If the TRN is active the business cannot skip filing.

A business that only supplies exempt goods or remains unregistered because it falls below the voluntary threshold will not need to file VAT returns.

UAE VAT Return Filing Periods and Deadlines

The FTA assigns each VAT-registered business a specific tax period, either monthly or quarterly, depending on its annual taxable turnover.

Quarterly Filing

Businesses with annual taxable revenue below AED 150 million follow a quarterly VAT return schedule. Returns must be submitted within 28 days after the end of each quarter:

- Q1 (January to March): Due by April 28

- Q2 (April to June): Due by July 28

- Q3 (July to September): Due by October 28

- Q4 (October to December): Due by January 28

Monthly Filing

Businesses with annual taxable revenue above AED 150 million follow a monthly filing cycle. Each return must be submitted by the 28th of the following month. For example, the return for May 2024 must be submitted by June 28, 2024.

FTA-Assigned Schedules

The FTA may assign a custom tax period depending on the business structure, activity level, or compliance track record. All tax periods and due dates are listed in the taxpayer’s EMARATAX account.

Details Required to File VAT 201 Return Form

To complete the VAT return filing in the UAE, every VAT-registered business must submit Form VAT 201 through the EMARATAX portal. This form captures the full breakdown of sales, purchases, VAT collected, and VAT paid during the tax period.

The portal accepts submissions online only. Taxpayers must enter the figures manually or upload the approved template with accurate and complete data.

Below is the list of sections included in VAT 201:

- Taxpayer Details

- VAT Return Period

- VAT on Sales and Other Outputs

- VAT on Expenses and Other Inputs

- Net VAT Due

- Additional Reporting Requirements

- Declaration and Authorised Signatory

Step-by-Step Process to File VAT Return in UAE

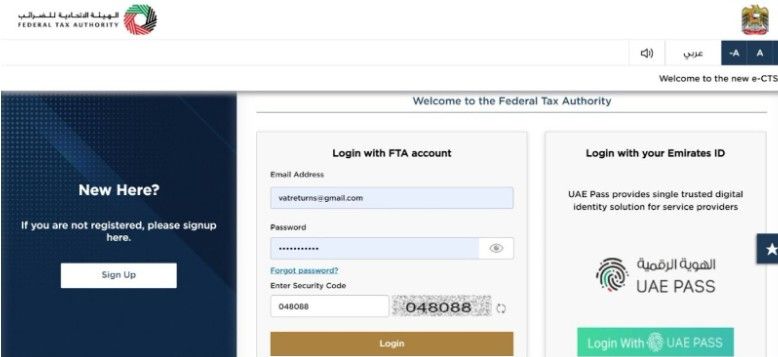

Step 1: Log in to the EMARATAX portal using your registered username and password.

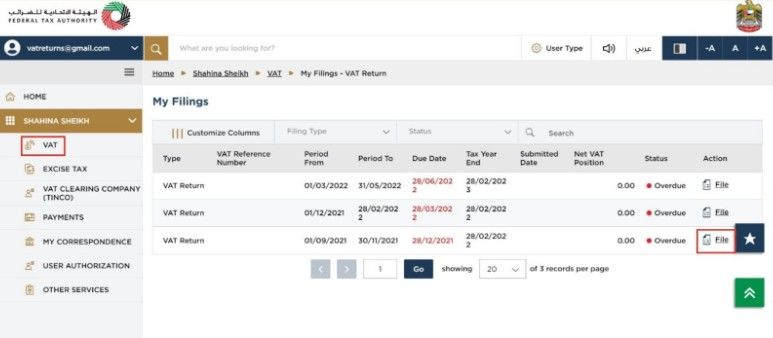

Step 2: Click on the navigation menu and go to:

VAT → View All under My Filings, then click on File for the relevant return period.

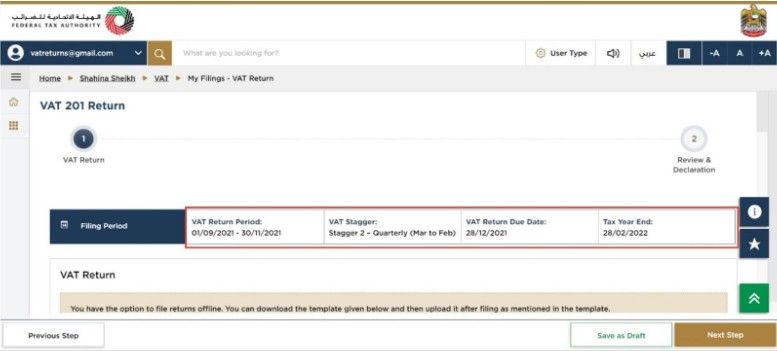

Step 3: Tick the checkbox to confirm the instructions and click the Start button to begin filing.

Step 4: The portal will display the VAT return period. You must review the period before moving forward.

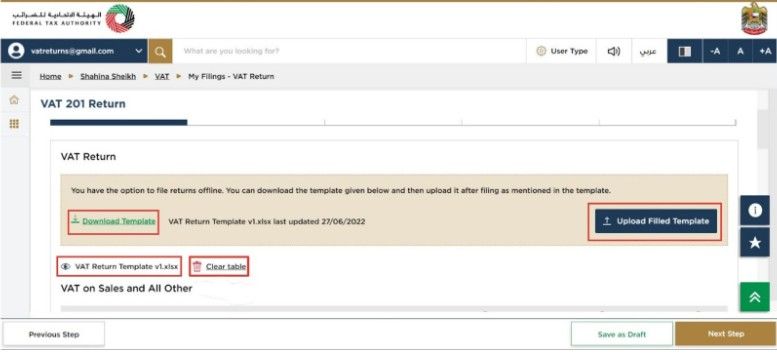

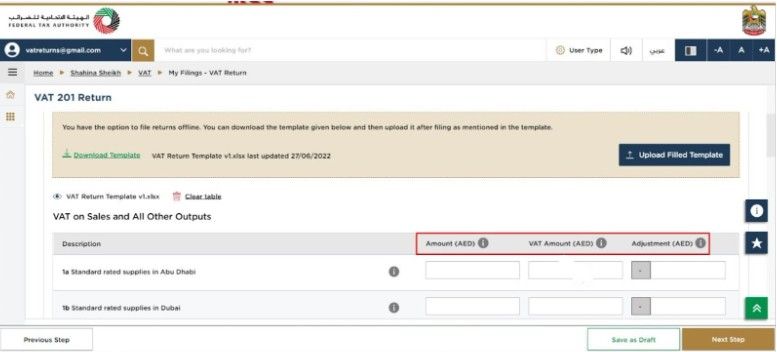

Step 5: You can download the offline Excel template to fill in your data. After entering the required details, upload the file. You can also download the uploaded Excel to check for any errors or clear it to upload a new file. (Optional)

Step 6: Enter the taxable amount, VAT amount, and adjustments in the respective fields.

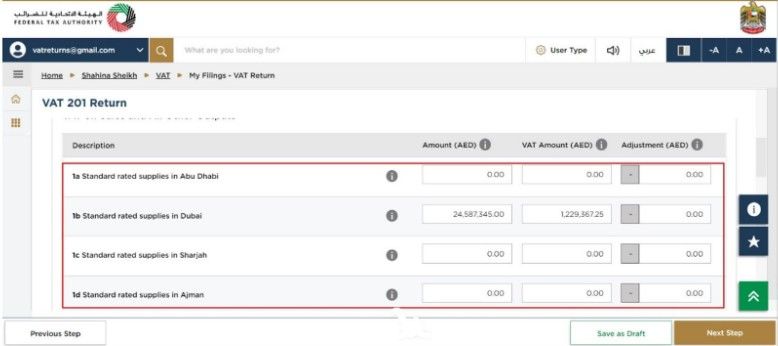

Step 7: Fill in Box 1 with standard-rated sales made to each emirate.

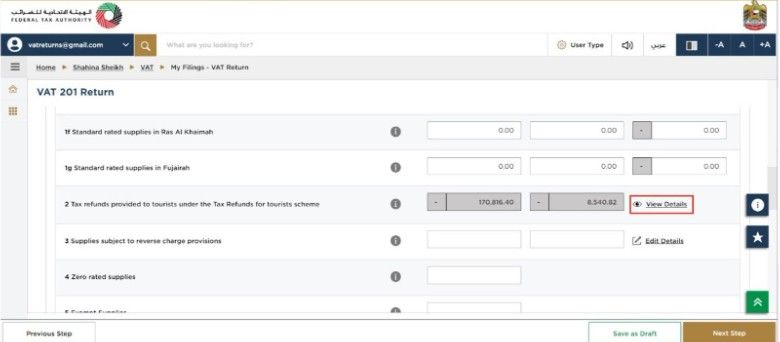

Step 8: Box 2 shows tourist VAT refunds auto-filled from the Planet Tax Free system. You can click on View Details To verify the values.

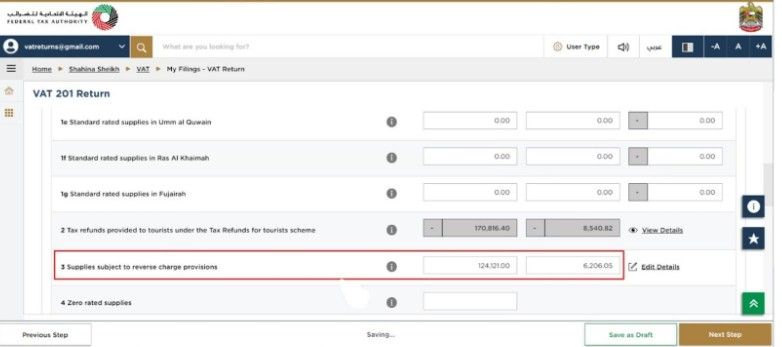

Step 9: Add reverse charge sales in Box 3.

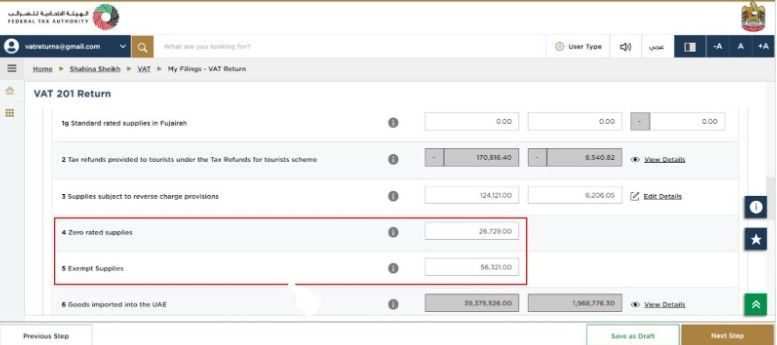

Step 10: Enter zero-rated sales in Box 4 and exempt sales in Box 5.

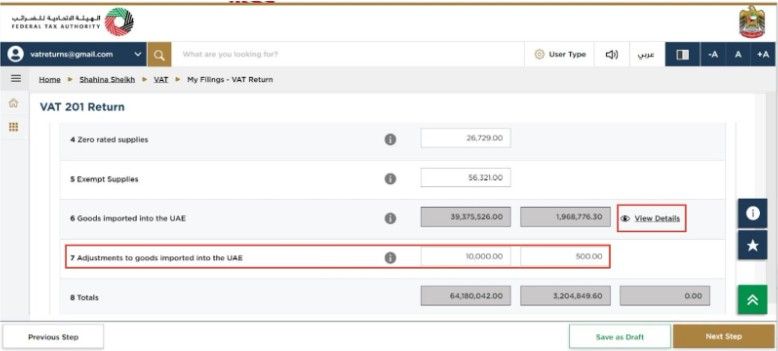

Step 11: Box 6 auto-fills with import data received from Customs. If any values are incorrect or missing, you can adjust them using Box 7.

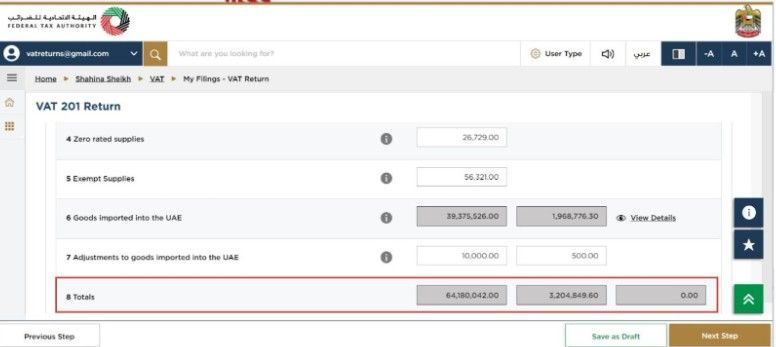

Step 12: Box 8 will show the total of Boxes 1 to 7 — this reflects your total sales and VAT liability.

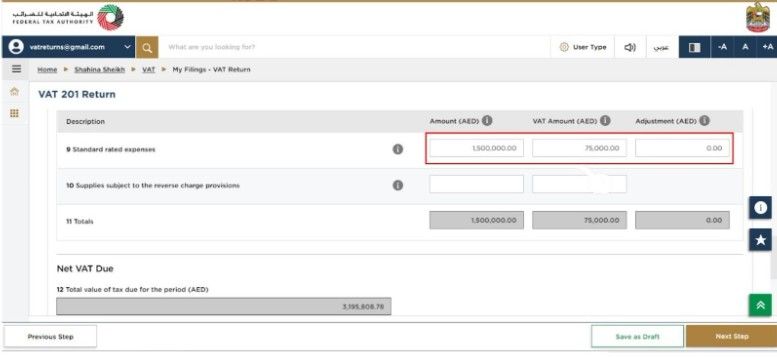

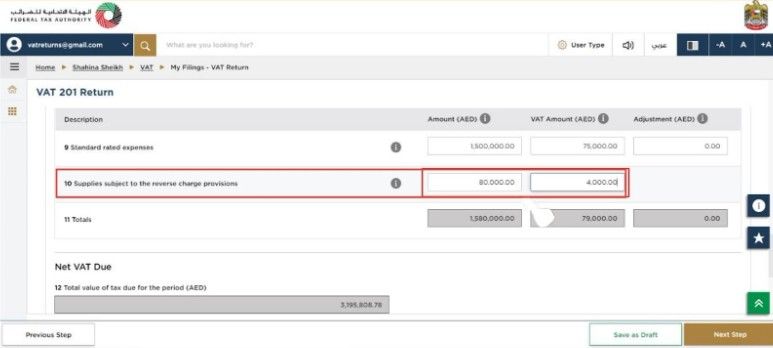

Step 13: Enter standard-rated expenses in Box 9, including amounts, VAT, and any adjustments.

Step 14: Report reverse charge purchases in Box 10.

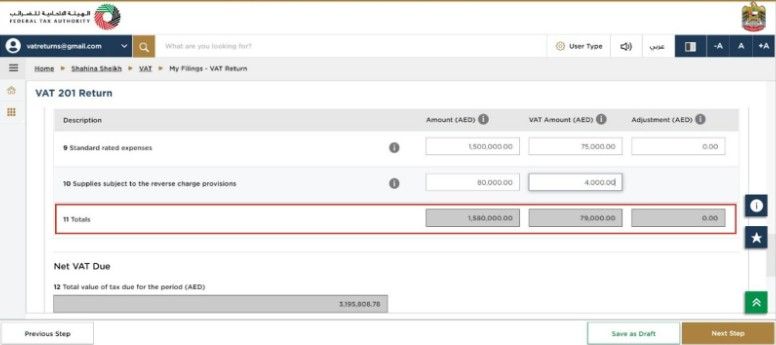

Step 15: Box 11 adds up the total inputs from Box 9 and Box 10.

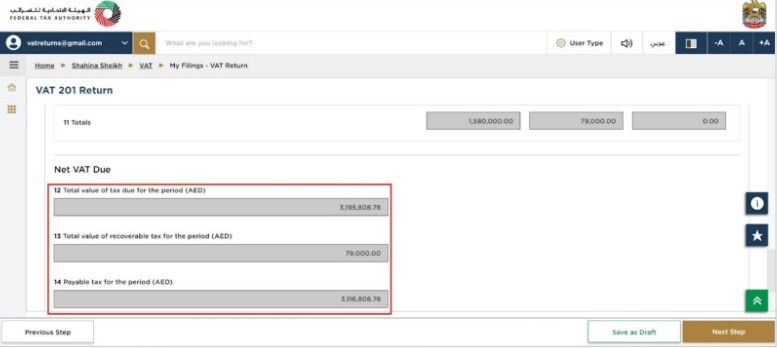

Step 16: Check Box 12 for output VAT and Box 13 for input VAT. Box 14 shows the VAT you must pay or the amount you can claim as a refund.

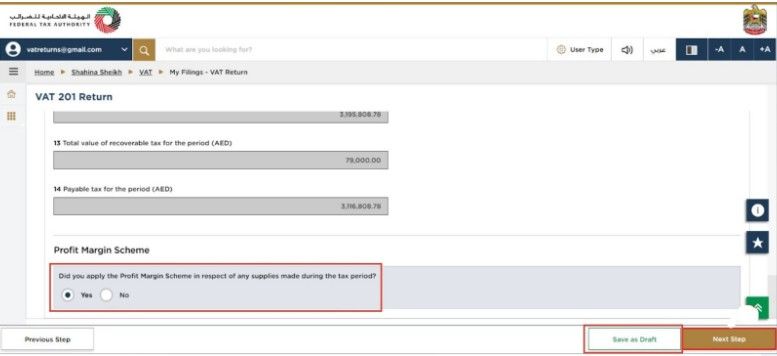

Step 17: Select Yes or No under the Profit Margin Scheme, based on what applies to your business. Click Save as Draft, then proceed by clicking Next Step.

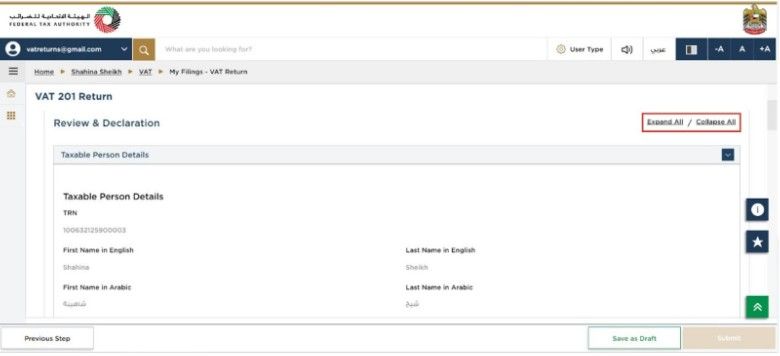

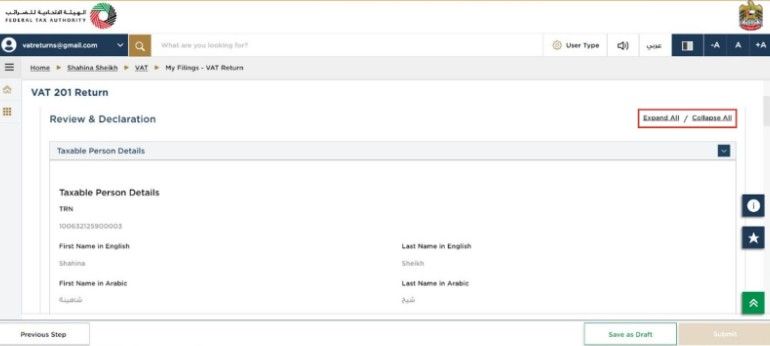

Step 18: Review the complete return. You can click on Expand All or Collapse All to check each section carefully before submission.

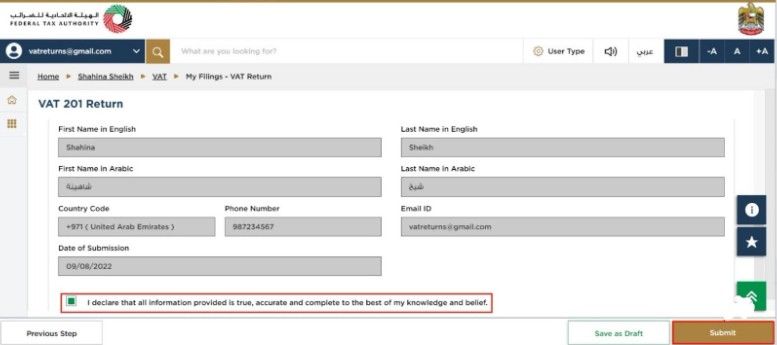

Step 19: Scroll down to the declaration section. Confirm the pre-filled details, tick the checkbox, and click Submit to file your return.

Step 19: Scroll down to the declaration section. Confirm the pre-filled details, tick the checkbox, and click Submit to file your return.

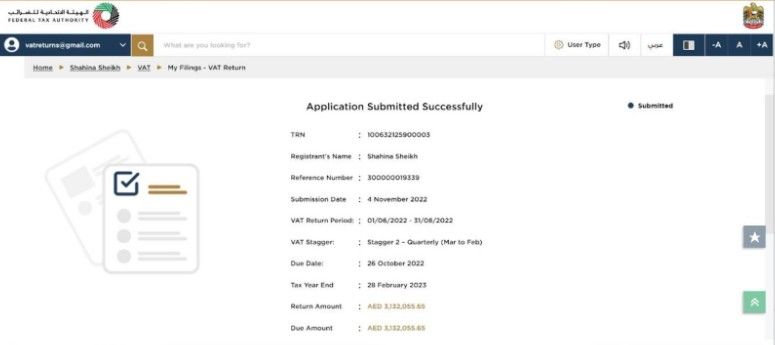

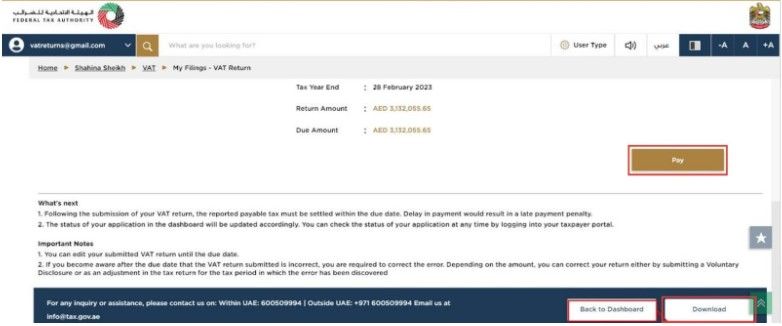

Step 20: After submission, the portal will show a confirmation screen with your reference number. Make a note of this for future use.

Step 21: You must complete the VAT payment before the due date. You can still edit the return before the deadline. Click on Download to save a copy of your VAT return acknowledgement.

Documents Required Before Filing VAT Return

Before filing your VAT return on the EMARATAX portal, you must keep all the required documents ready. These records help you enter correct values and avoid errors during filing.

Here are the key documents you need:

- VAT Registration Certificate

Shows your Tax Registration Number (TRN) and proves that your business is VAT registered. - Trade License

This proves your business holds a valid license to operate in the UAE. - Tax Invoices

Keep copies of all tax invoices issued to customers and received from suppliers. These help report both sales and expenses correctly. - Financial Records

Prepare your bank statements, debit and credit notes, and expense reports. These records support the values you report in the return. - Customs Documents

If you import or export goods, keep all customs declarations and shipping documents ready. These help calculate VAT on imports and confirm exports.

Common Penalties for VAT Return Filing in the UAE

The Federal Tax Authority (FTA) imposes fines for delays, errors, and missing records. The table below shows common violations and the penalties that apply:

| Violation | Penalty |

| Late filing of VAT return | AED 1,000 (first offense), AED 2,000 (repeat within 24 months) |

| Late VAT payment | 2% immediately, 4% after 7 days, 1% daily after 1 month (up to 300%) |

| Incorrect VAT return filing | AED 1,000 (first offense), AED 2,000 (repeat) |

| Incorrect VAT return (voluntary disclosure) | 50%, 30%, or 5% of unpaid VAT (based on timing of disclosure) |

| Failure to submit VAT voluntary disclosure | AED 3,000 (first time), AED 5,000 (repeat) |

| Failure to keep financial records | AED 10,000 (first offense), AED 50,000 (repeat) |

| Failure to submit documents in Arabic | AED 20,000 |

| Failure to support or allow FTA audits | AED 20,000 |

Quick Navigation

Book a Demo

Learn more by booking a demo with our team. We'll guide you step by step.